For small and medium businesses, invoice mistakes may look minor at first. A wrong GSTIN, incorrect tax rate, missing HSN code, or mismatch between invoice and return data can create bigger problems later. Customers may not be able to claim Input Tax Credit. Payments may get delayed. The accounts team may spend extra time correcting entries. In some cases, the business may receive notices or face penalties.

Most invoice errors do not happen because businesses are careless. They happen because GST invoicing has many moving parts: customer details, place of supply, tax rates, HSN/SAC codes, invoice numbering, e-invoicing, e-way bills, credit notes, debit notes, and return matching.

The good news is that most of these mistakes can be avoided with a disciplined process and the right accounting system.

1. Incorrect or Missing GSTIN

One of the most common GST invoice mistakes is entering the wrong GSTIN of the customer or supplier. This usually happens because GSTINs are copied from old records, typed manually, or not verified before invoice generation.

A wrong GSTIN can create problems for both parties. The buyer may not see the invoice correctly reflected for Input Tax Credit. The seller may face reconciliation issues during return filing. If the customer’s GSTIN is inactive, cancelled, or linked to a different state, the invoice may need correction later.

Businesses should verify customer GSTINs before adding them to the billing system. Once verified, the GSTIN should be stored in the customer master record so that the same error is not repeated.

Good practice: Maintain an updated customer master with GSTIN, legal name, trade name, billing address, shipping address, state, and place of supply details.

A business owner or accountant reviewing GST invoices on a laptop, ensuring checklist items are met.

2. Wrong HSN or SAC Code

HSN codes are used for goods, while SAC codes are used for services. These codes help classify the supply and determine reporting accuracy.

Using the wrong HSN or SAC code can lead to incorrect tax treatment, mismatched records, and confusion during filing. Many businesses use approximate codes or copy codes from previous invoices without confirming whether they are still appropriate.

This is especially common in businesses that sell multiple product categories or provide bundled services. For example, a business dealing in hardware, software, installation, and support services may need different classifications depending on the nature of supply.

Businesses should not treat HSN/SAC codes as a one-time setup. Product and service masters should be reviewed periodically, especially when new items are added.

Good practice: Map each product or service to the correct HSN/SAC code in your accounting system and restrict manual editing during invoice creation.

3. Applying the Wrong GST Rate

Incorrect GST rate selection is another frequent issue. A product may be taxed at 5%, 12%, 18%, or another applicable rate depending on classification and notification updates. Some supplies may be exempt, nil-rated, or subject to special conditions.

Mistakes usually happen when rates are selected manually or when businesses continue using old rates after changes. Another common problem is applying the same rate to all items in a mixed invoice, even when different items attract different rates.

Wrong tax rates affect invoice value, tax liability, customer records, and return filing. If the mistake is discovered late, the business may need to issue a credit note or debit note.

Good practice: Keep tax rates linked to product/service masters instead of selecting rates manually for every invoice.

4. Confusion Between CGST, SGST, and IGST

Whether to charge CGST + SGST or IGST depends mainly on the place of supply and the location of the supplier and recipient.

For intra-state supplies, CGST and SGST are generally applied. For inter-state supplies, IGST is generally applied. But businesses often make mistakes when billing customers across states, shipping goods to a different location, or handling services where place of supply rules need careful attention.

This mistake can be costly because the total tax amount may look correct, but the tax type may be wrong. For example, charging CGST and SGST instead of IGST can create return filing and reconciliation issues.

Good practice: Do not rely only on the billing address. Check supplier state, recipient state, shipping address, and place of supply before finalizing the invoice.

5. Irregular Invoice Numbering

GST invoices should follow a proper serial numbering system. Problems arise when businesses skip numbers, repeat invoice numbers, use different formats without control, or manually edit invoice numbers.

Irregular numbering creates confusion during audits, return filing, and payment reconciliation. It also makes it difficult to track cancelled invoices, revised invoices, and credit notes.

This issue is common when multiple people generate invoices from different systems or when sales invoices are created manually outside the accounting software.

Good practice: Use system-generated invoice numbers with a consistent format for each financial year, branch, or business unit.

6. Missing Mandatory Invoice Details

A GST invoice should contain key details such as supplier information, GSTIN, invoice number, invoice date, recipient details, description of goods or services, HSN/SAC, taxable value, tax rate, tax amount, place of supply where applicable, and signature or digital authorization.

When invoices are created manually, some of these details may be missed. Even a well-designed invoice template can create problems if important fields are left blank.

Incomplete invoices may affect customer confidence and create issues during accounting, ITC matching, and audit verification.

Good practice: Use a standard GST invoice template and make important fields mandatory in the billing system.

7. Not Linking Credit Notes and Debit Notes Properly

Credit notes and debit notes are part of normal business operations. They may be required for sales returns, rate differences, quantity differences, discounts, short billing, or invoice corrections.

The problem starts when credit notes and debit notes are issued without clear reference to the original invoice. This makes reconciliation difficult for both seller and buyer.

For example, if a customer returns part of an order, the credit note should clearly mention the original invoice details and reason for adjustment. Without this, accounts teams may struggle to match the transaction later.

Good practice: Always link credit notes and debit notes to the original invoice number and maintain proper reasons for adjustment.

8. Delay in Invoice Creation

Some businesses create invoices after goods are dispatched or after services are completed, but delay the actual billing entry. This can affect accounting accuracy, stock records, e-way bill coordination, payment follow-up, and return filing.

Delayed invoicing also creates confusion for customers. They may receive goods or services but not receive the invoice on time, which can delay payment processing.

For service businesses, late invoice creation can also affect revenue tracking and cash flow visibility.

Good practice: Create invoices as part of the sales or dispatch workflow, not as a month-end activity.

9. Invoice and E-Way Bill Mismatch

For goods movement where an e-way bill is required, invoice details and e-way bill details should match. Mismatches in invoice number, date, vehicle number, value, GSTIN, place of delivery, or item details can create issues during transport checks.

Many mismatches happen because invoice data is entered in one system and e-way bill data is entered separately. Manual re-entry increases the chance of mistakes.

Good practice: Where possible, generate e-way bills using invoice data from the accounting system to reduce duplication and errors.

10. Ignoring E-Invoicing Requirements

Businesses covered under e-invoicing must generate invoices in the prescribed manner and obtain the required invoice reference details before treating the invoice as valid for applicable transactions.

A common mistake is generating a regular invoice in accounting software but not completing the e-invoice process where it is applicable. Another mistake is assuming that e-invoicing applies to every transaction in the same way. Applicability may depend on turnover, transaction type, and notified rules.

Businesses should regularly check whether e-invoicing applies to them, especially when turnover grows.

Good practice: If your business is close to the e-invoicing threshold, prepare early. Do not wait until the last week of the financial year to change your invoicing process.

11. Poor Record Keeping and Reconciliation

GST invoice management does not end when an invoice is issued. Businesses must also maintain records for payments, receipts, returns, amendments, credit notes, debit notes, and customer communication.

Poor record keeping leads to month-end pressure. The accounts team may need to compare sales registers, bank statements, GST returns, e-way bills, e-invoices, and customer ledgers manually. This is where many errors are discovered late.

Good practice: Reconcile invoices regularly instead of waiting for return filing deadlines. Weekly review is better than monthly panic.

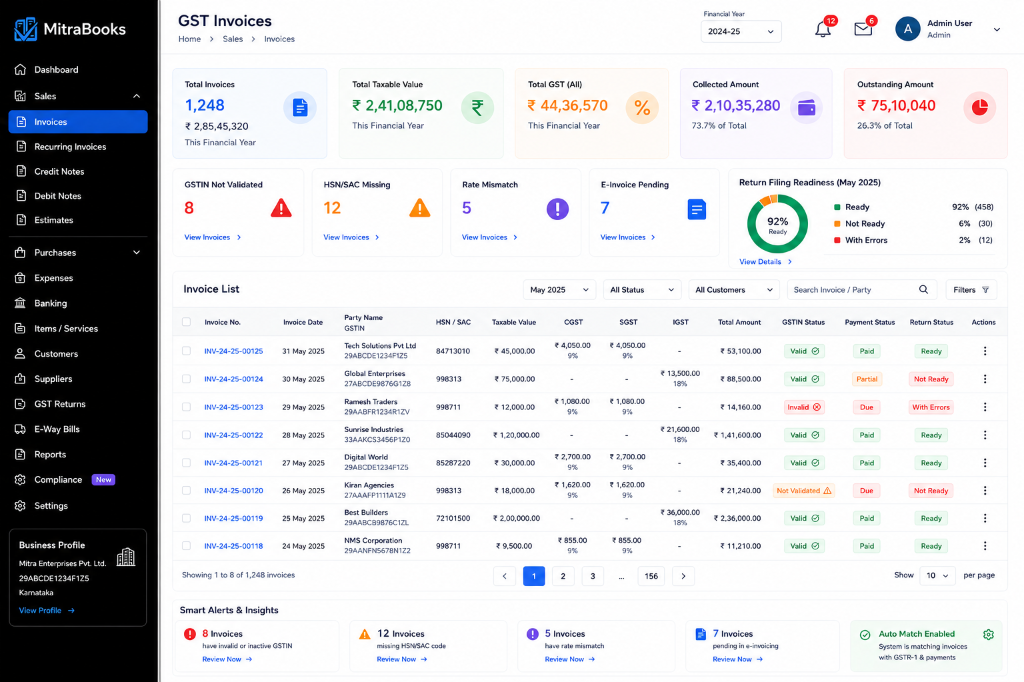

A clean MitraBooks GST invoice management dashboard showing invoice lists, validation status, tax amounts, and compliance alerts.

12. Using Spreadsheets for Too Long

Spreadsheets are useful in the early stage of a business, but they become risky as invoice volume increases. Manual formulas, copied templates, multiple versions, and uncontrolled editing can create serious errors.

A spreadsheet may not validate GSTIN, prevent duplicate invoice numbers, track credit notes properly, calculate tax based on rules, or generate reports needed for compliance.

At some stage, businesses need a proper accounting and GST billing system. Applications like MitraBooks can help businesses manage invoices, GST details, customer records, payment status, reports, and accounting workflows in one place. This reduces manual effort and improves reliability.

Practical Checklist Before Issuing a GST Invoice

Before finalizing a GST invoice, businesses should check:

- Is the customer GSTIN correct and active?

- Is the billing and shipping address correct?

- Is the place of supply correctly selected?

- Are CGST, SGST, and IGST applied correctly?

- Are HSN/SAC codes accurate?

- Are tax rates updated?

- Is the invoice number correct and unique?

- Are taxable value, discount, and tax amount calculated correctly?

- Is the e-way bill required?

- Is e-invoicing applicable?

- Are payment terms clearly mentioned?

- Is the invoice saved and backed up properly?

A simple checklist can prevent many avoidable mistakes.

Conclusion

GST invoice management is not just a compliance task. It directly affects cash flow, customer trust, Input Tax Credit, return filing, and audit readiness.

Most invoice mistakes are avoidable if businesses follow a clear process, maintain accurate master data, review tax rates, validate GSTINs, and use reliable accounting software.

For growing businesses, digital invoice management is no longer optional. It saves time, reduces errors, improves compliance, and gives the business better control over its financial records. A clean invoice today can prevent a complicated problem tomorrow.